Saving for a down payment can feel like the biggest hurdle when buying a home. And with affordability still a challenge, it's easy to wonder how people are making it happen. But here's something that might surprise you.

Some people are getting into homes with a smaller down payment.

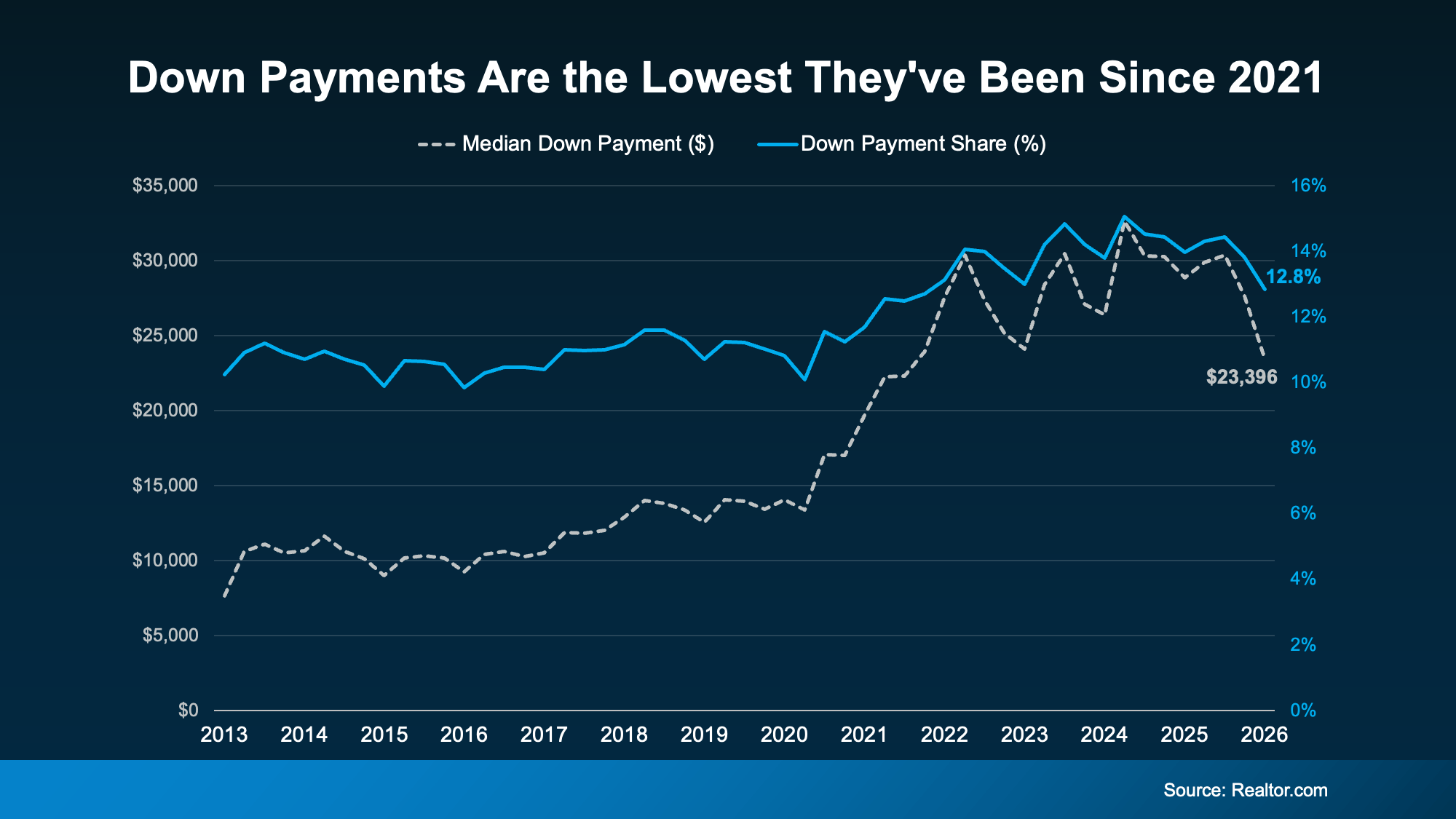

According to Realtor.com, the typical buyer put down about $23,400 in early 2026. That's about $5,000 less than the year before, a 19% drop. In fact, it's the lowest typical down payment we've seen since 2021, as the graph below shows.

So why are buyers putting less money down? And how can you do the same? Here's what you need to know.

Why Down Payments Are Getting Smaller

There are a few reasons behind this trend.

One is that the market is more balanced. With less competition from other buyers, there's less pressure to make a large down payment just to stand out.

Another reason is that home prices are growing more slowly. Since your down payment is based on the purchase price, slower price growth or even slight price drops in some markets can mean you need less money upfront.

More buyers are also choosing loan programs with lower down payment requirements. Government-backed loans like FHA and VA loans can require very little or even no money down, making homeownership more accessible for many buyers.

Even with a smaller down payment, it's still a big expense and saving that kind of money isn't always easy. So how do buyers make it work? For many, the answer comes down to taking advantage of homebuyer assistance programs and getting a little help from family or loved ones.

Help You May Not Know You Qualify For

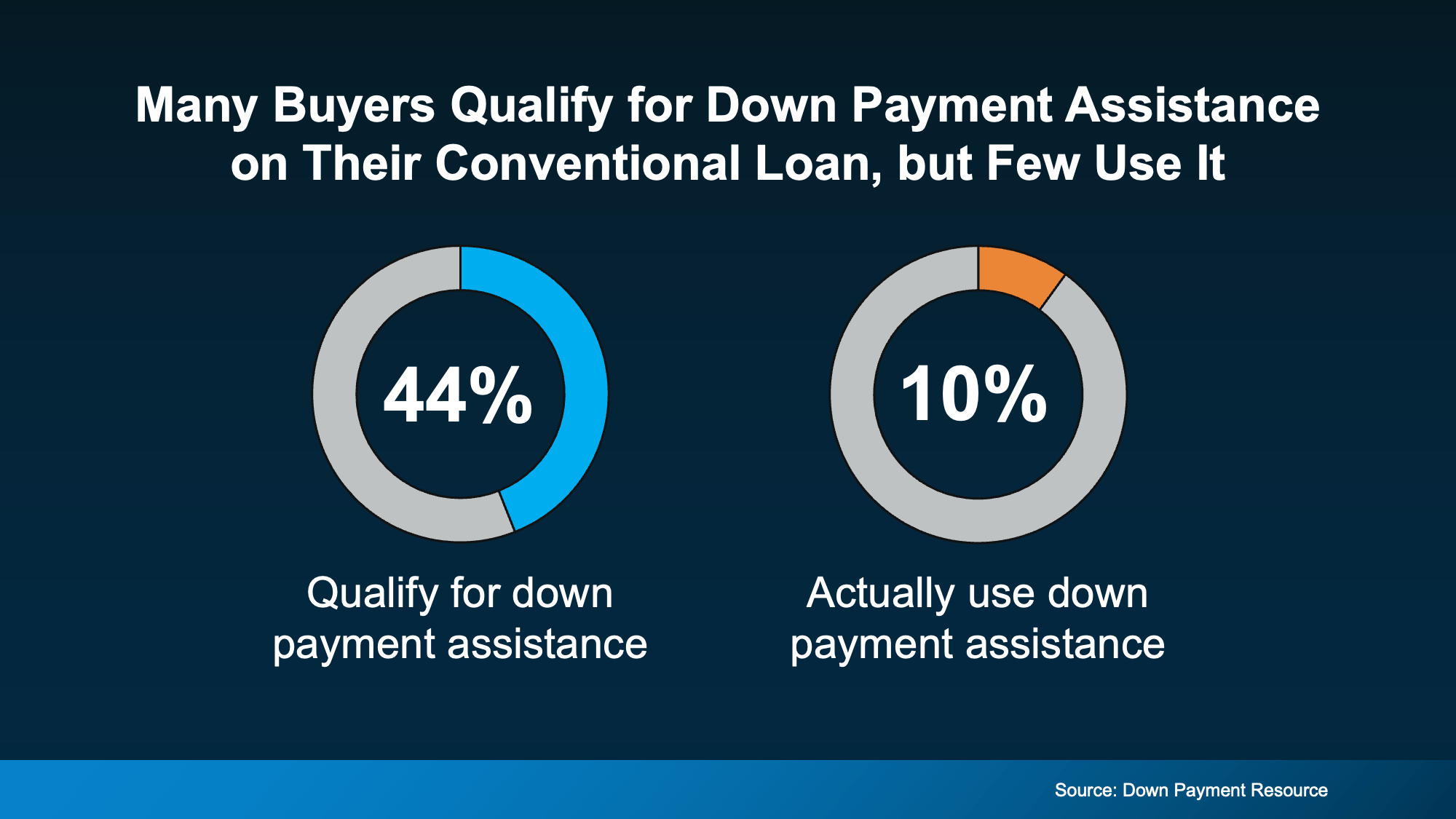

Down payment assistance is one of the best kept secrets for homebuyers. A recent study from Urban Institute and Down Payment Resource found that nearly 44% of buyers in the 10 largest U.S. metro areas qualified for a down payment assistance program. Even so, many of them bought a home without ever taking advantage of that help, as the chart below shows.

The good news is there are more options than most people realize. According to Down Payment Resource:

More than 2,600 down payment assistance programs are available across the country.

About 62% are designed for first time homebuyers.

Around 38% don't require you to be a first time buyer, so you may still qualify even if you've owned a home before.

And 62% are available to buyers earning $100,000 or more.

A Boost from Loved Ones

For many buyers, the help starts a little closer to home. According to Veterans United, about 59% of parents have either helped or plan to help their children financially when it comes to buying a home.

That support is most often used for the down payment, but it can also help buyers qualify for a mortgage or cover closing costs. As Chris Birk, VP of Mortgage Insight at Veterans United, explains:

““For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

”

If your loved ones can help, it can really speed up how soon you’re able to buy.

Bottom Line

Down payments are smaller than they've been in years, making it easier for more buyers to take the next step toward homeownership.

And when you combine down payment assistance programs with a little help from loved ones, buying a home may be more within reach than you think. Connect with a trusted lender to explore your options and see what's possible.