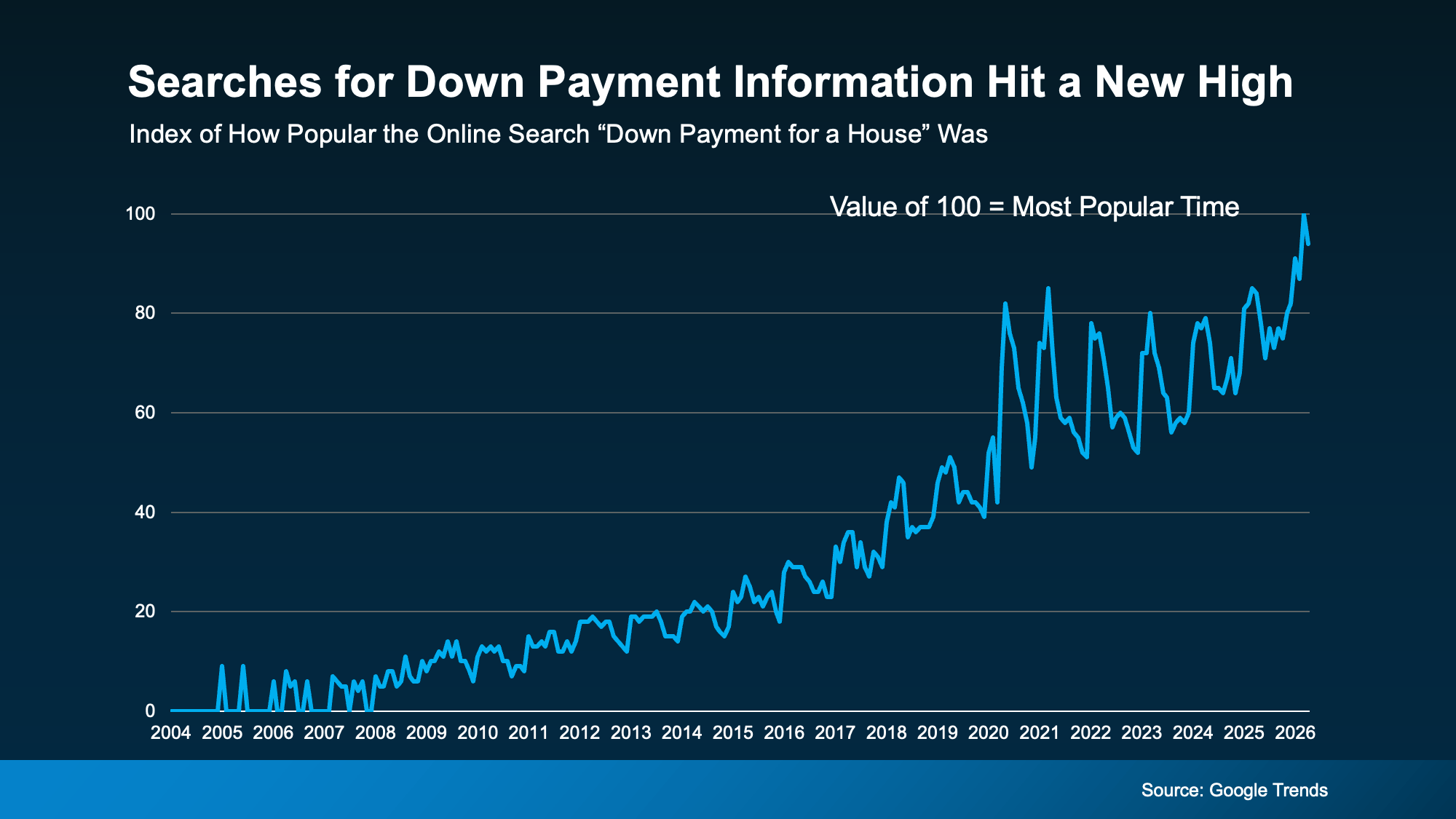

According to Google Trends, searches for down payment information have recently reached an all time high. That tells us more buyers are actively trying to understand how much they really need to save before taking the next step, as shown in the graph below.

If you’re asking yourself the same question, you can definitely search online for answers. But most of the time, it makes more sense to talk to a local expert. Here’s what a pro would likely tell you.

The 20% Down Payment Myth

A lot of people still believe you need 20% down to buy a home, but that’s one of the biggest myths out there. The data actually shows that’s not the case.

While there are definitely advantages to putting that much down, most first-time buyers actually put down a lot less.

Here’s the thing. Unless your lender specifically requires it, you usually don’t have to put 20% down. In fact, there are loan options out there that are designed to help you buy a home with a much smaller upfront cost. As The Mortgage Reports explains:

““The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

”

For example, FHA loans allow you to put down as little as 3.5%. And if you qualify, VA and USDA loans can even offer zero down payment options, including for eligible Veterans.

And that’s one of the reasons so many first-time buyers are able to purchase a home without putting 20% down.

What Buyers Are Actually Putting Down

So if buyers aren’t putting 20% down, what are they actually putting down instead?

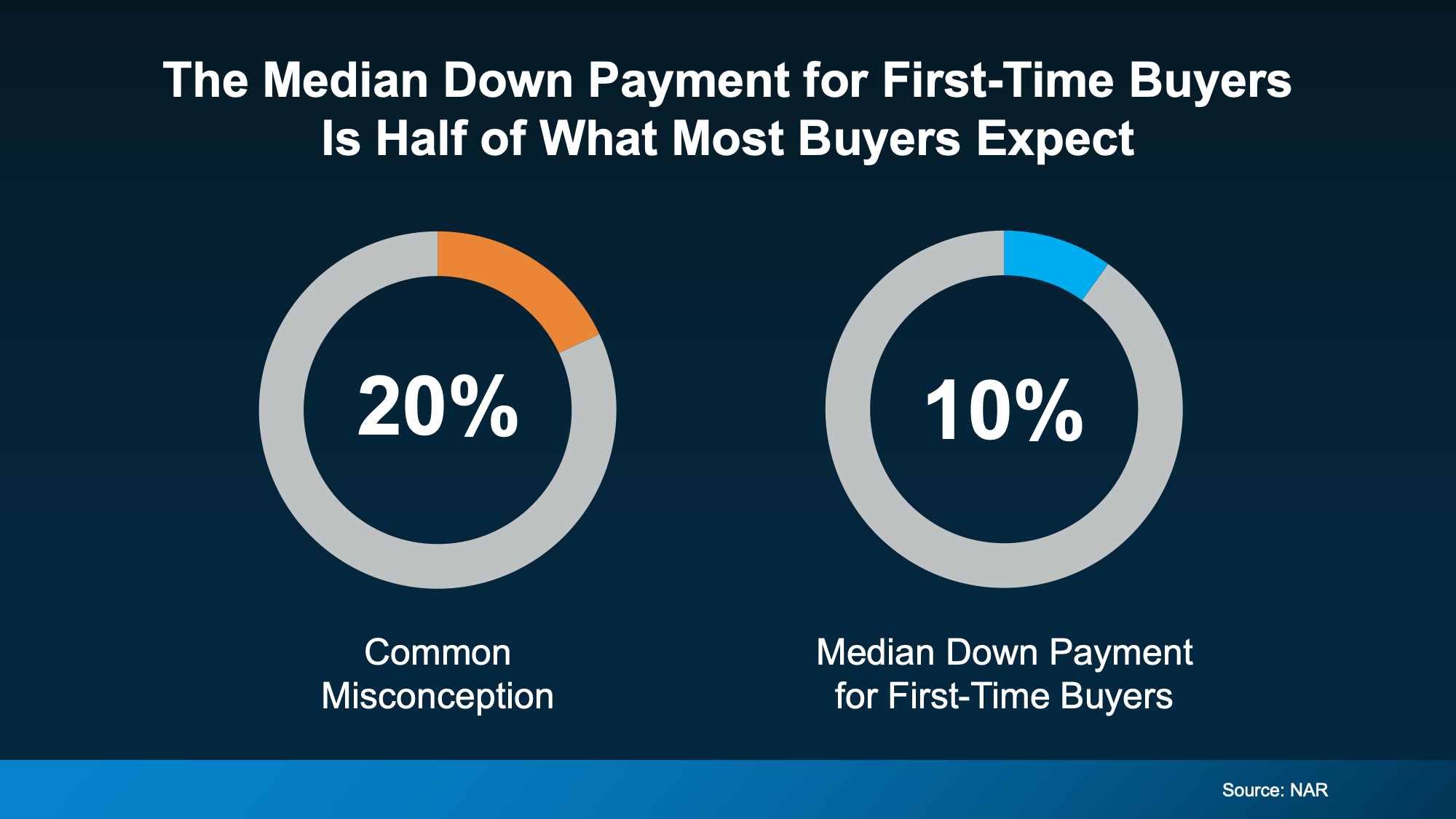

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is just 10%. That’s only half of what most people usually expect.

That means if you’re trying to save 20% because you think it’s required, you might actually be planning for a longer timeline than you really need.

And here’s even better news. Not only might you be able to buy a home with less money down than you expected, but there are also options that can help you reach your down payment goal faster.

Why You Should Look into Down Payment Assistance Programs

There are many programs that can help you save for a down payment, and they can really speed up how quickly you reach your goal. Many buyers don’t know how many options exist or that they might qualify for assistance.

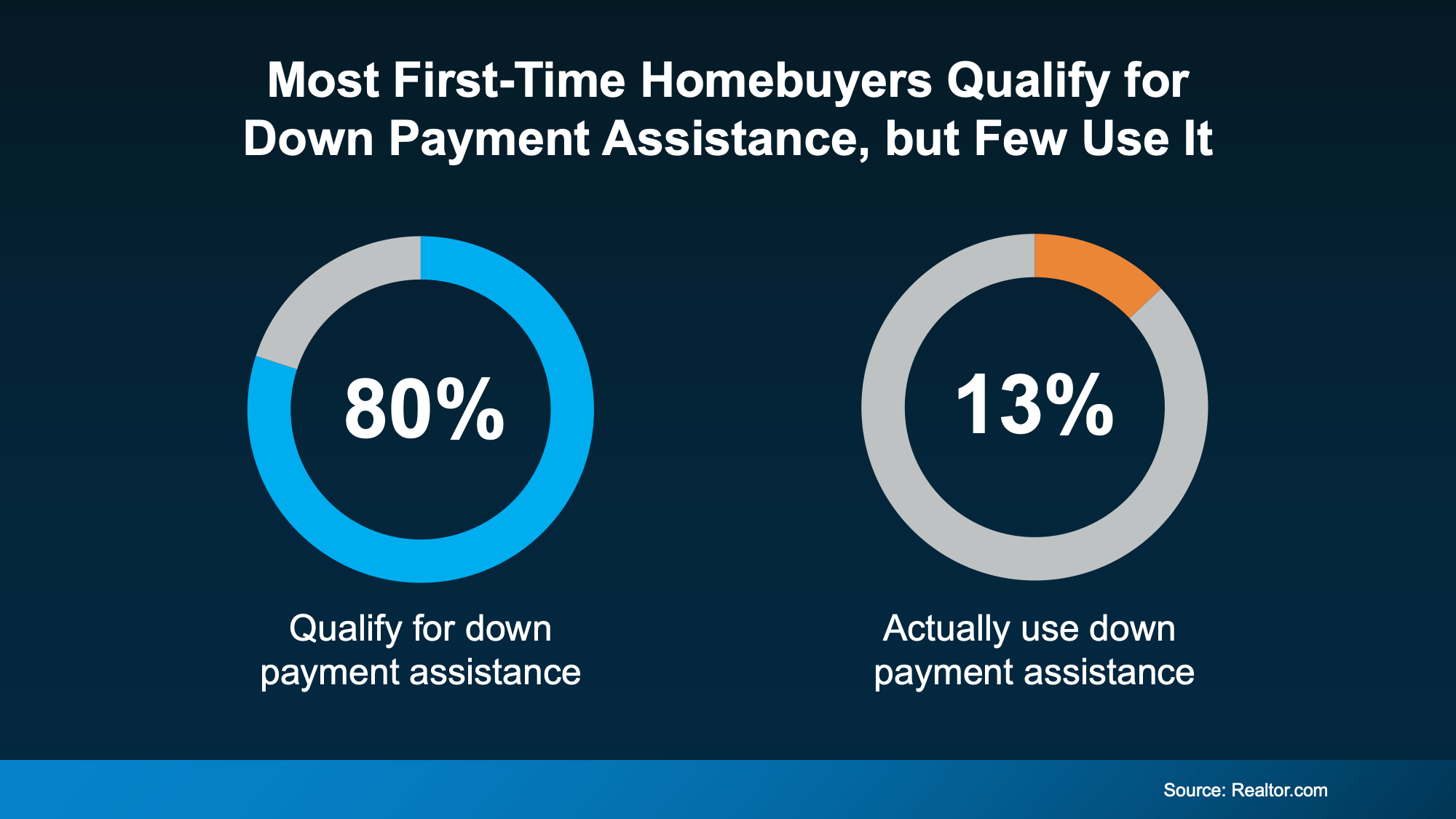

Research from Realtor.com shows that nearly 80% of first-time homebuyers qualify for down payment assistance programs, but only about 13% actually take advantage of them, as shown in the chart below.

And that’s another missed opportunity that could be holding some buyers like you back.

In the U.S., there are more than 2,600 homeownership programs available, and many of them offer meaningful financial help. As Down Payment Resource shares:

““With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

”

Just imagine how much further your savings could stretch with an extra $18,000 to help you buy a home. In some cases, you might even be able to combine multiple programs, giving your savings an even bigger boost.

Bottom Line

The simple truth is, most first-time buyers aren’t putting 20% down. And if you’ve been waiting to reach that amount before buying, you might be stretching out your timeline more than you actually need to.

To figure out what you actually need to save and see if you qualify for any assistance, it helps to talk with a trusted lender who can walk you through your options. You might be able to buy a home sooner than you think.