If you’ve been watching the housing market and waiting for a sign that affordability is improving, this may be the one you’ve been looking for. In just the past year, mortgage rates have dropped by about a full percentage point — and that shift can make a meaningful difference in what homeownership costs.

While headlines often focus on whether rates are still “high,” what matters most is how changes in rates affect your monthly payment and long-term savings. And right now, the math is working more in buyers’ favor than it was a year ago.

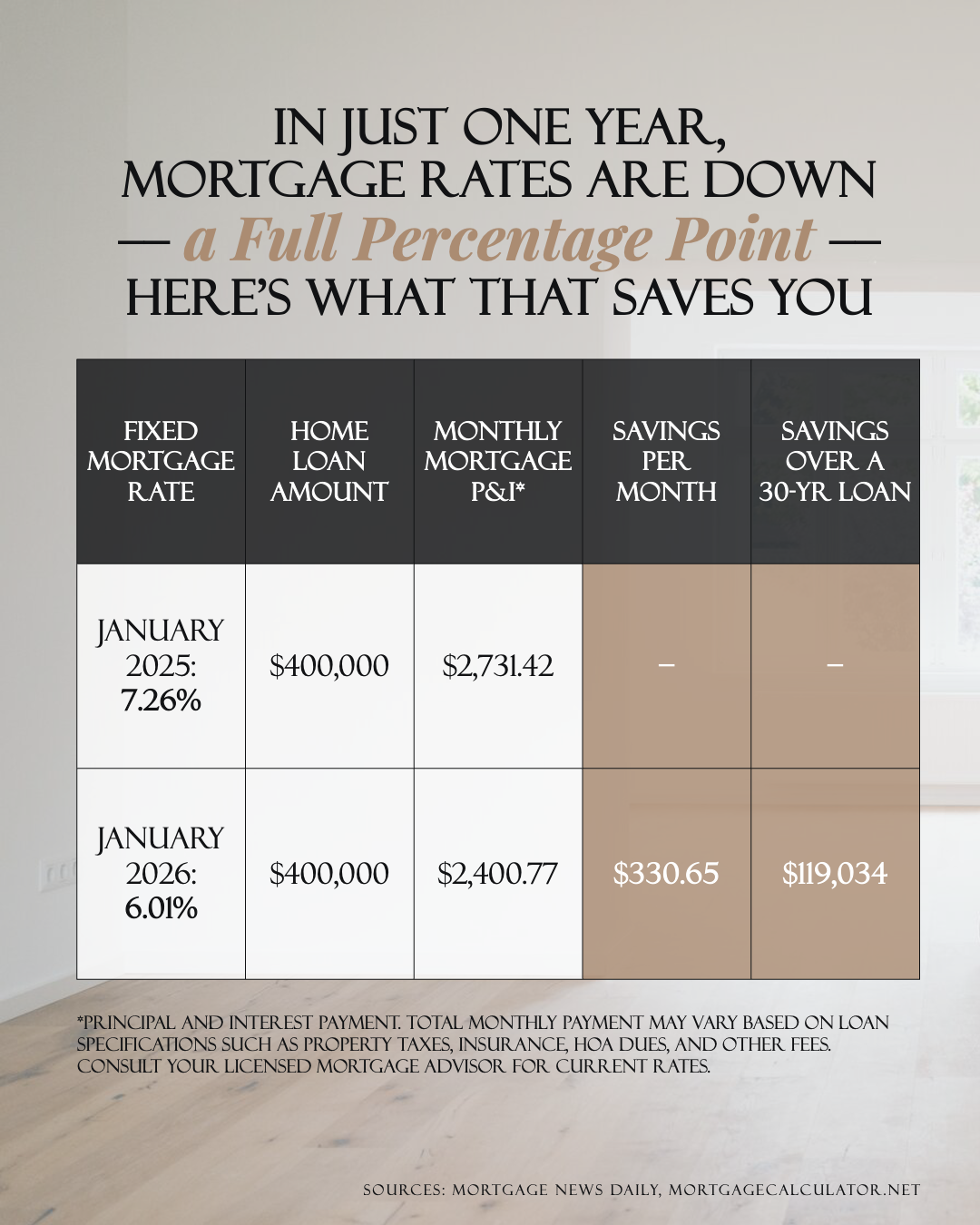

What a 1% Drop in Rates Really Means

A one-percentage-point change may not sound dramatic at first, but over time, it adds up in a big way.

For example, on a $400,000 home loan:

At a 7.26% rate (January 2025): the monthly principal and interest payment would be about $2,731.

At a 6.01% rate (January 2026): that payment drops to roughly $2,401.

That’s a savings of about $330 every month — or more than $119,000 over the life of a 30-year loan.

Even small shifts in rates can significantly impact your buying power and your long-term financial picture.

Why This Matters for Today’s Buyers

Lower mortgage rates can help in several important ways:

Improved affordability: Lower monthly payments make it easier to fit a home into your budget.

More purchasing power: Some buyers may qualify for a higher-priced home without increasing their monthly payment.

Greater flexibility: Savings can be redirected toward repairs, furnishings, investments, or simply peace of mind.

If you stepped back from the market because payments felt too high last year, it may be worth taking another look.

What About Waiting for Rates to Drop Even More?

Trying to time the market perfectly is tough. While rates could fluctuate, today’s lower levels already represent a meaningful improvement from where they were a year ago.

And remember: if rates drop further in the future, refinancing could be an option — but waiting too long could mean missing out on the right home or facing increased competition if more buyers jump back in at once.

The Bottom Line

Mortgage rates don’t need to return to historic lows to make a difference. A one-percentage-point drop has already created real savings for buyers, both monthly and long-term.

If you’ve been holding off on buying because of affordability concerns, now may be a smart time to revisit your options and see what today’s rates mean for you.