If you’ve been house hunting lately, you’ve probably noticed how challenging affordability still feels. And that’s a big reason why more buyers are turning to adjustable rate mortgages, also known as ARMs, to help make the numbers work.

Here’s what you should know about how they work and whether they could be a good fit for you.

What Is an Adjustable-Rate Mortgage?

Because a lot of people aren’t very familiar with this type of loan, let’s start with a simple definition. Here’s how Business Insider explains the key difference between a fixed rate mortgage and an adjustable rate mortgage.

““With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

”

Basically, you don’t change much over the life of your loan.

And one of them can change over time, sometimes just a little and sometimes by quite a bit.

Of course, things like taxes or homeowner’s insurance can still affect a fixed rate loan, but the base portion of your mortgage payment usually stays pretty steady. The big difference is that with an ARM, your monthly payment can change as time goes on.

Why Adjustable-Rate Mortgages Are Getting More Attention

So why do some buyers choose this option? It’s simple, they’re attracted to the lower upfront costs. Here’s how Business Insider puts it.

““Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

”

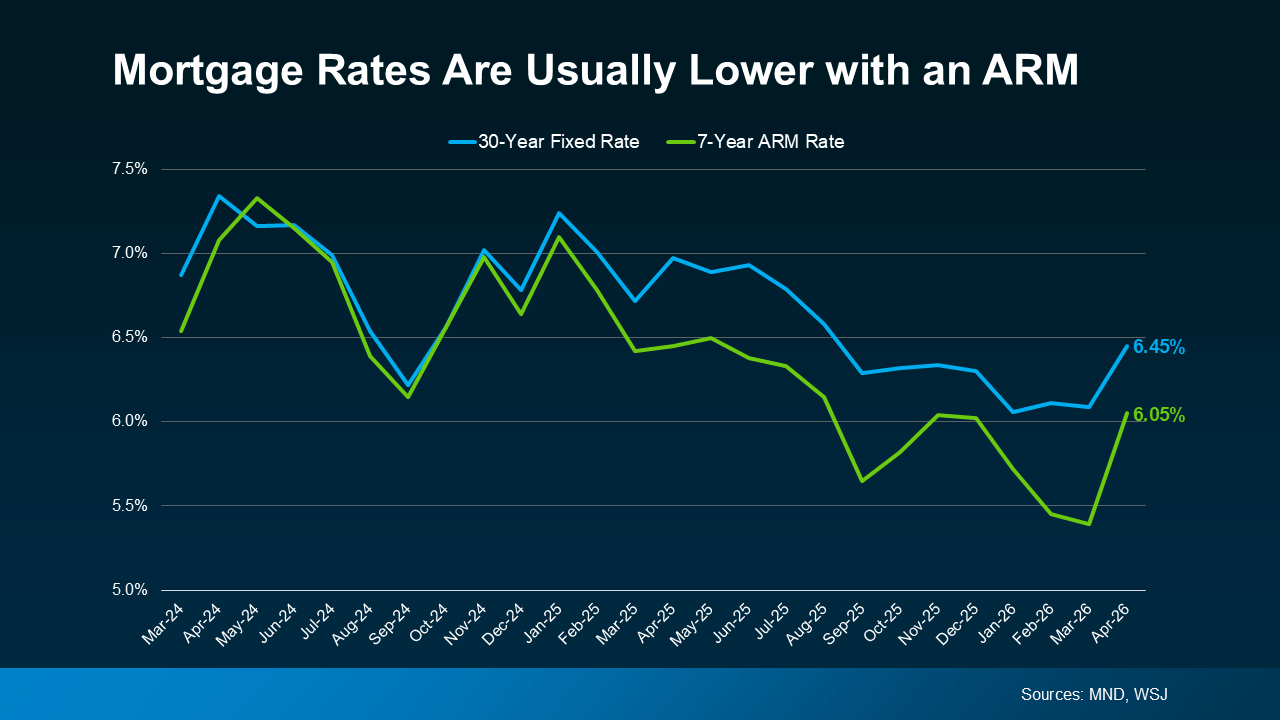

And right now, according to Mortgage News Daily and the Wall Street Journal, the starting rate on an ARM is lower than what you’d typically see with a 30 year fixed mortgage, as shown in the graph below.

If you’re curious how that translates to actual dollars, Redfin’s research shows the typical buyer might save around $150 a month by choosing an ARM instead of a 30-year fixed mortgage.

For some people, that’s all it takes to make a difference.

More Buyers Are Choosing Adjustable-Rate Mortgages Today

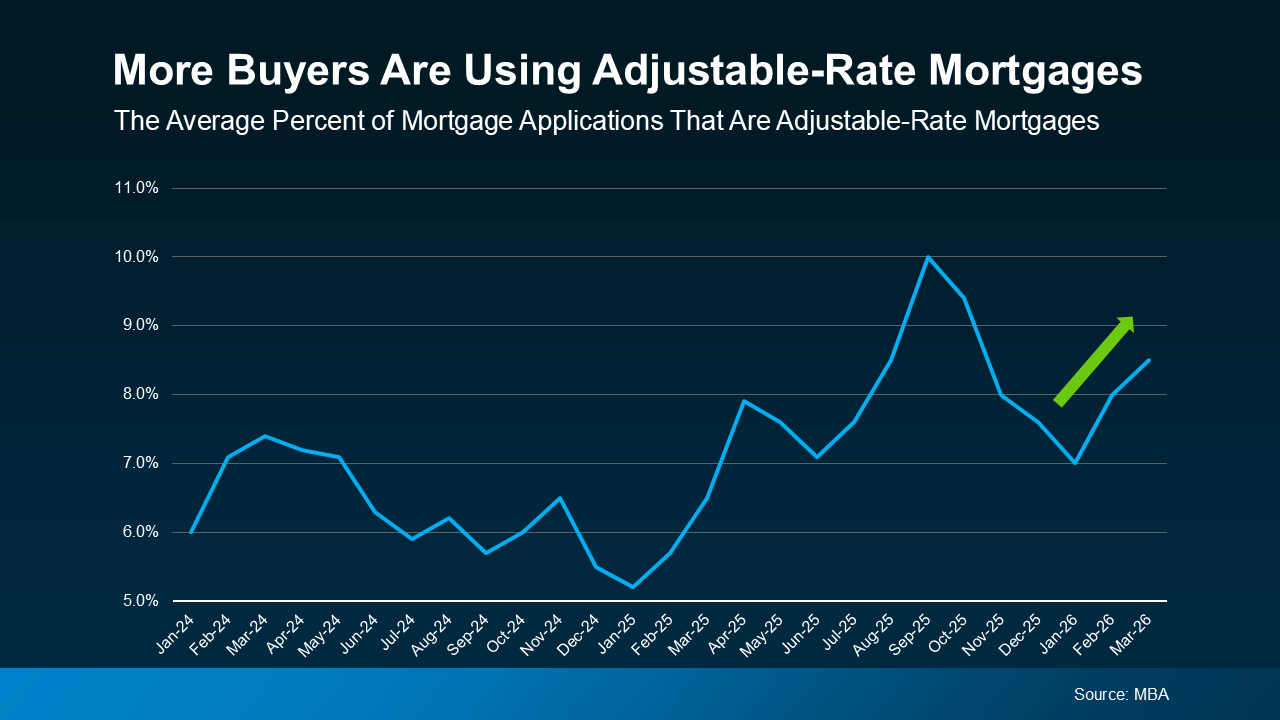

More buyers are choosing to take on a bit of uncertainty down the road in exchange for a lower monthly payment right now. Data from the Mortgage Bankers Association shows that the share of people using ARMs has been rising, especially in the past few years, as you can see in the graph below.

This doesn’t mean adjustable-rate mortgages are the best choice for everyone. It simply means some buyers are choosing them so they can still purchase a home today.

If you remember the housing crash, the rise of adjustable-rate mortgages might worry you. But don’t—today’s ARMs are different.

Back then, some buyers ended up with loans they couldn’t afford once the rates changed.

Today, lending standards are a lot stricter, and lenders make sure borrowers could still afford the payment even if rates go up. So the return of ARMs isn’t a sign of another housing crash. It simply shows how some buyers are adjusting to today’s affordability challenges.

The Trade-Off – What You Need To Consider

If you’re thinking about an adjustable rate mortgage, it really comes down to your personal situation and how comfortable you are with taking on some risk.

An ARM could make sense if you’re planning to move before the rate changes or if you expect your income to be higher in the future. But there are still some trade-offs you’ll want to carefully consider.

And it’s also important to remember there’s no guarantee mortgage rates will drop in the future, so refinancing later may not always be possible. That’s why it really matters to think about your overall plan, consider your long term income potential, and talk it through with a trusted lender before deciding on an ARM.

Bottom Line

Adjustable-rate mortgages are drawing more interest again since they can make buying a home more affordable initially, but they aren’t the best choice for everyone.

The key is knowing how they work, what the risks are, and whether they fit your plan. That’s why you should talk with a trusted lender and a financial advisor before making any decisions.