Mortgage rates have already dipped into the upper 5% range twice this year. But after only a few days, they moved back up into the low 6% range. If you saw that and thought, “Great, I missed it,” you’re definitely not the only one.

A lot of buyers are treating the 5% range like it’s some kind of magic number. Like going from 6.1% to 5.99% suddenly changes everything. And mentally, it really can feel different.

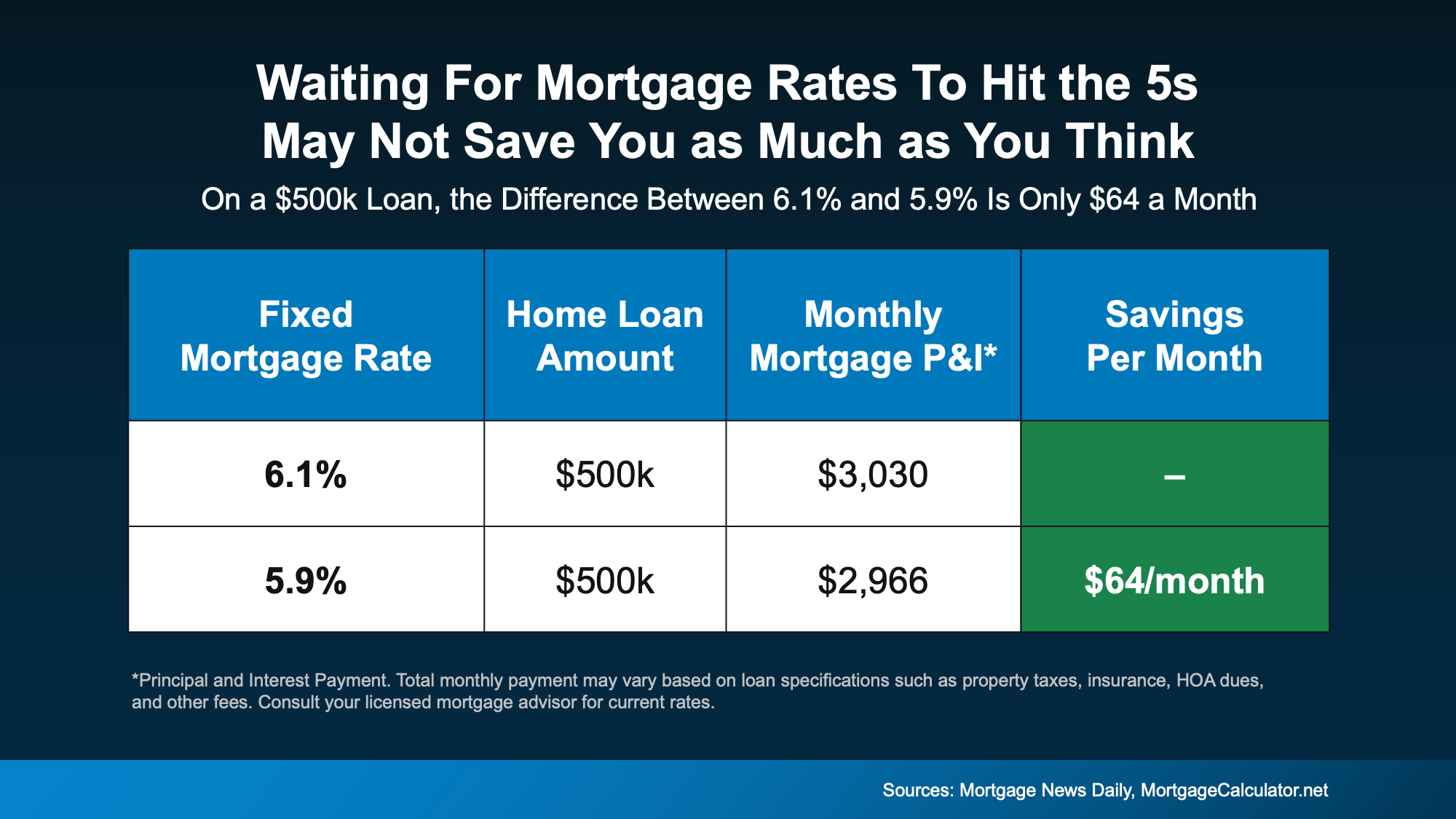

But here’s the part most people don’t usually stop to do the math on.

The Payment Difference Isn’t What You Think

Let’s say you’re looking at a $500,000 home loan. At 6.1%, your principal and interest payment would be around $3,030 a month. At 5.9%, it drops to about $2,966 a month.

That’s only a $64 difference per month.

Not $300.

Not $500.

Just sixty dollars.

Take a second and let that sink in.

Yes, over time that $64 a month can add up. But it’s nowhere near the dramatic change many buyers picture when they say they’re waiting for rates to get into the 5s.

Seeing a 5 at the start of your rate can feel like a big deal mentally. The actual financial impact? In the end, it might be barely noticeable.

Experts Aren’t Predicting a Big Drop

Another thing to keep in mind is that most housing economists don’t expect rates to stay in the 5% range anytime soon.

Rates will bounce up and down, probably hitting the high 5s now and then, but most experts expect them to stay around the low 6% range this year rather than drop back into the 5s or fall much further.

It could happen, sure, but the reality is that waiting for a big drop might not give you the payoff you’re hoping for if you’re holding out.

The Bigger Question to Ask

Instead of asking, “Did I miss the 5s?” it’s better to ask, “Does this payment work for me?”

If the monthly payment fits comfortably in your budget and you’ve found a home that works for you, the difference between 6.1% and 5.9% probably isn’t a dealbreaker. It might be a small factor, but it shouldn’t be the whole decision.

And keep in mind, mortgage rates aren’t set in stone. If they drop significantly later, you can always refinance. But you can’t refinance a home you haven’t bought yet.

Waiting Might Feel Safe, But It Isn’t Always Strategic

It’s natural to want the best rate possible—everyone does. But sometimes buyers overestimate how much a rate in the high 5s will actually make a difference in today’s market.

Don’t forget that rates have already dropped. A year ago, they were in the 7s. Now they’re sitting in the low 6s. For many people, that full percentage point difference is already the real game changer.

If you put your plans on hold when rates were higher, now might be a good time to run the numbers again. Not because rates are “perfect,” but because your monthly payment might be more manageable than you expect, even with rates in the low 6s.

Before you assume you’ve missed your chance, take another look at the numbers.

You might find it never went away.

Bottom Line

If you've been waiting on the sidelines for mortgage rates to hit a "perfect" number, that approach may not be as advantageous as you think.

Let’s connect so you can double-check the math on your price point, you might find the payments are already within your range.