Renting might feel like the easier option right now. There’s no large down payment to come up with. No unexpected repair bills to worry about. And no long-term commitment tying you down.

But then your rent goes up. And then it goes up again. All of a sudden, what once felt flexible starts to feel really expensive, especially when you realize you’re not building any equity in the process. And when that hits, it’s easy to feel stuck in the cycle.

There’s so much talk right now about how buying a home just isn’t affordable. But the truth is, when you actually look at the numbers, they may make a lot more sense than you’d expect based on what’s changed lately.

Buying Is More Affordable Than Renting in Many Areas

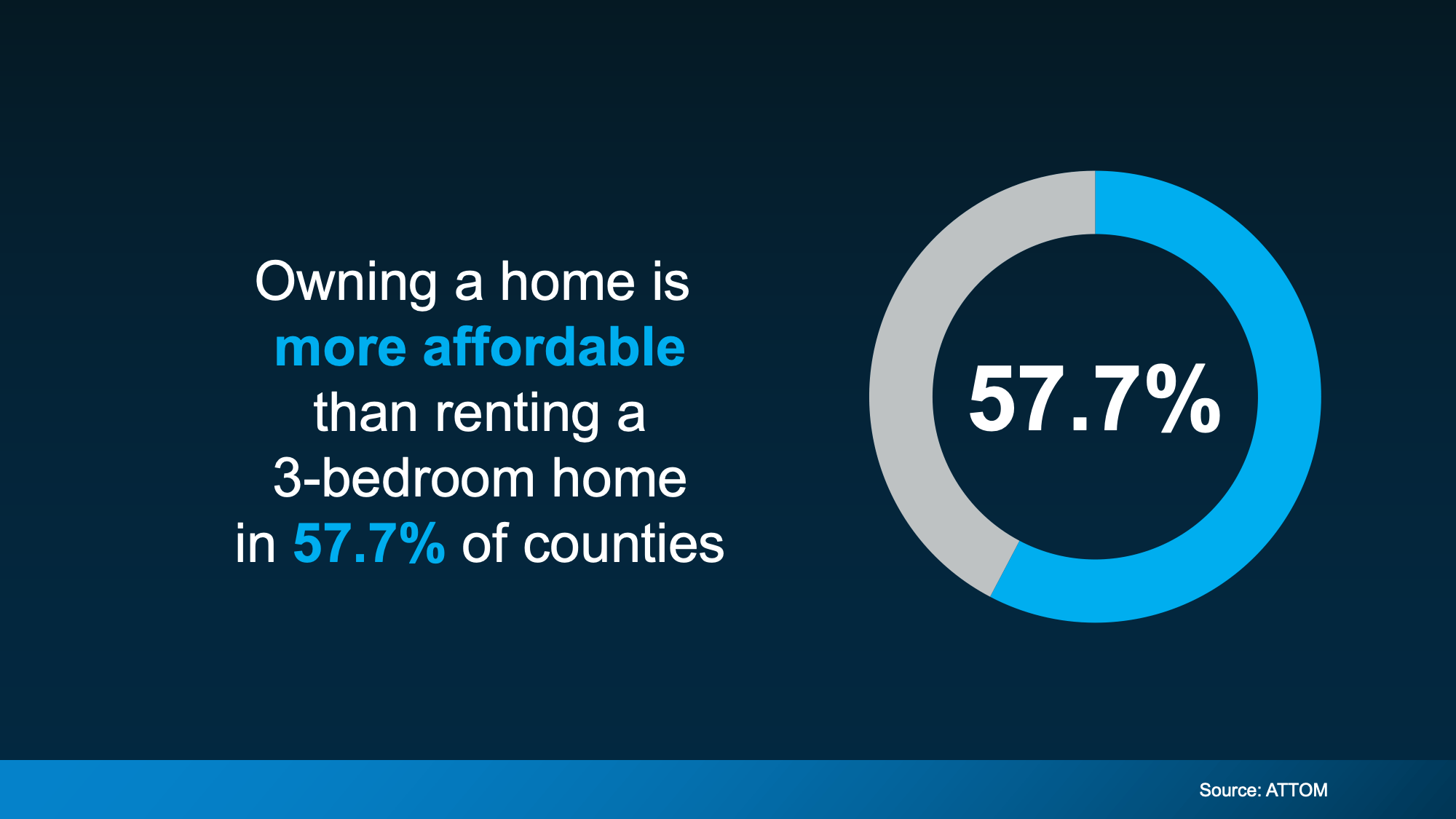

In many places today, owning a home can cost less each month than renting a three-bedroom house. Recent data from ATTOM shows this is the case in nearly 58% of U.S. counties (see chart below).

And that’s after you factor in things like insurance and normal maintenance costs.

Even if it feels surprising, the numbers show that rent often strains monthly budgets more than owning does. That’s because home prices are rising more slowly, there are more homes for sale, and monthly mortgage payments are starting to ease as interest rates fall.

Affordability Still Varies by Region

Now, even though things have shifted nationally, that doesn’t automatically mean buying is more affordable in every market or for every renter.

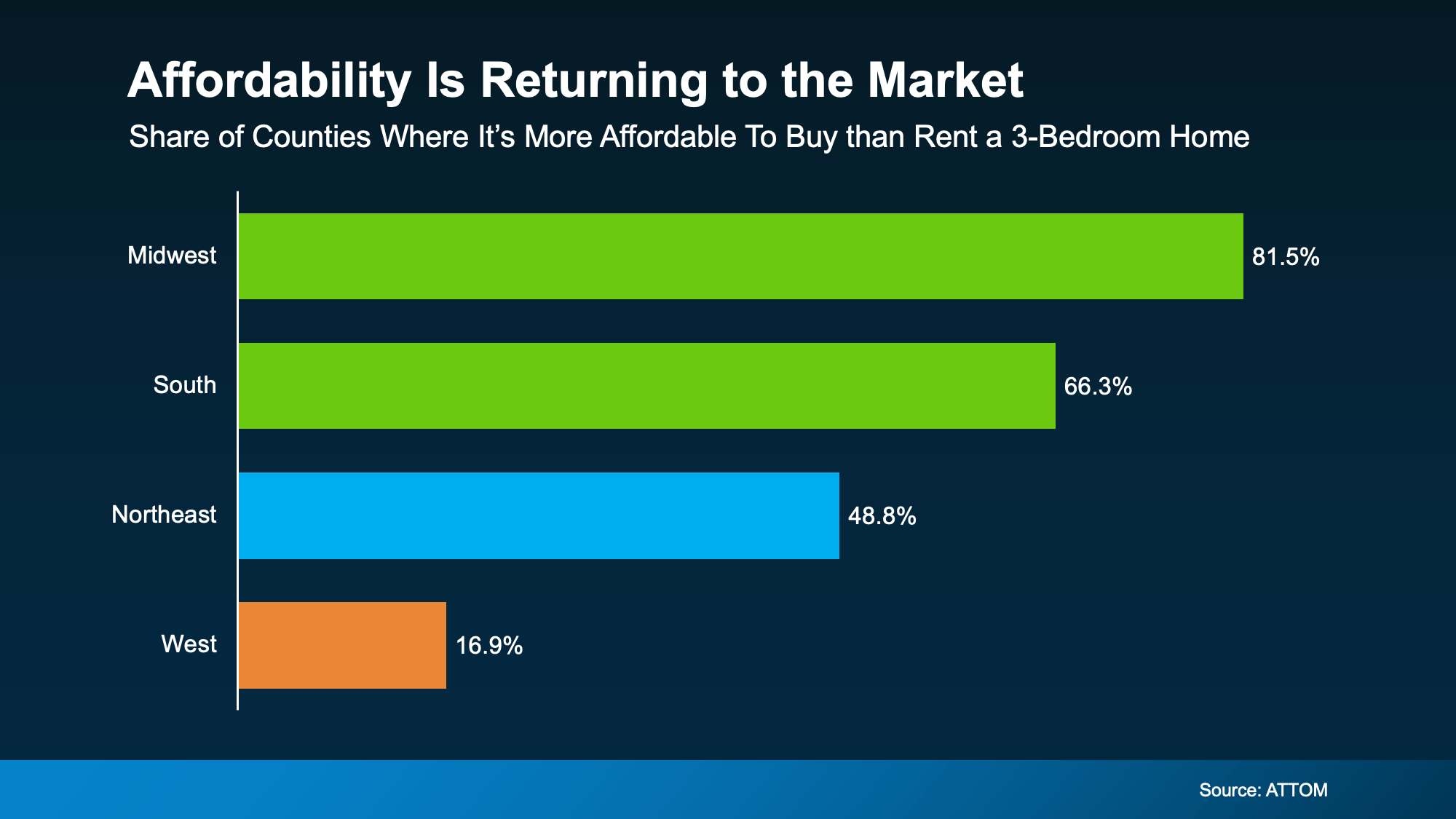

Buying is cheaper than renting in about 58% of U.S. counties, but the numbers vary a lot by region (see graph below).

The biggest improvements are happening in the Midwest and South, but if you live in the West, things may still feel tight.

The takeaway is that how affordable buying is really depends on where you live. The only way to know for sure is to look at the numbers in your local area.

So, What’s Still Holding Buyers Back?

Maybe you’re following along but still thinking, “Okay, but I still can’t afford the upfront costs.” If so, you’re not alone.

For many renters, the toughest part isn’t just the monthly payment — it’s coming up with the down payment.

You’re not out of options. The part most people don’t hear enough about is that there are thousands of down payment assistance programs across the country, and many buyers qualify without even knowing it.

And the average benefit? Roughly $18,000.

That support can help pay part of your down payment or closing costs, so you might not have to save as much as you think to get started.

When you factor in monthly payments that could be more manageable than you expect, especially with rates easing and prices cooling, buying may feel a lot more realistic than it seems at first.

Bottom Line

The point isn’t that everyone needs to rush out and buy a home tomorrow.

Renting isn’t always cheaper than it seems, and once you consider the full picture, buying can often be more attainable than it feels.

If you’re renting and feel stuck in the “someday” loop, have a quick conversation to see what’s possible and whether it makes sense for you.