If you’ve read headlines about foreclosures rising for 10 straight months, it’s natural to worry that the housing market is in trouble. But the full story is more nuanced — a few straightforward facts put the trend into better context:

Foreclosure levels today are right where they’re expected to be — nothing out of the ordinary.

Thanks to strong home equity, most homeowners are still in a solid financial position.

And there’s nothing in the data that suggests a surge of distressed sales or a market crash is on the horizon.

Foreclosure Filings Are Up 32%, But That Doesn’t Mean the Market’s in Trouble

At the heart of it, people worry we might see a repeat of 2008 — when risky lending and too many homes on the market pushed prices down and triggered a wave of foreclosures that hurt lots of families. But this time around, the conditions are different.

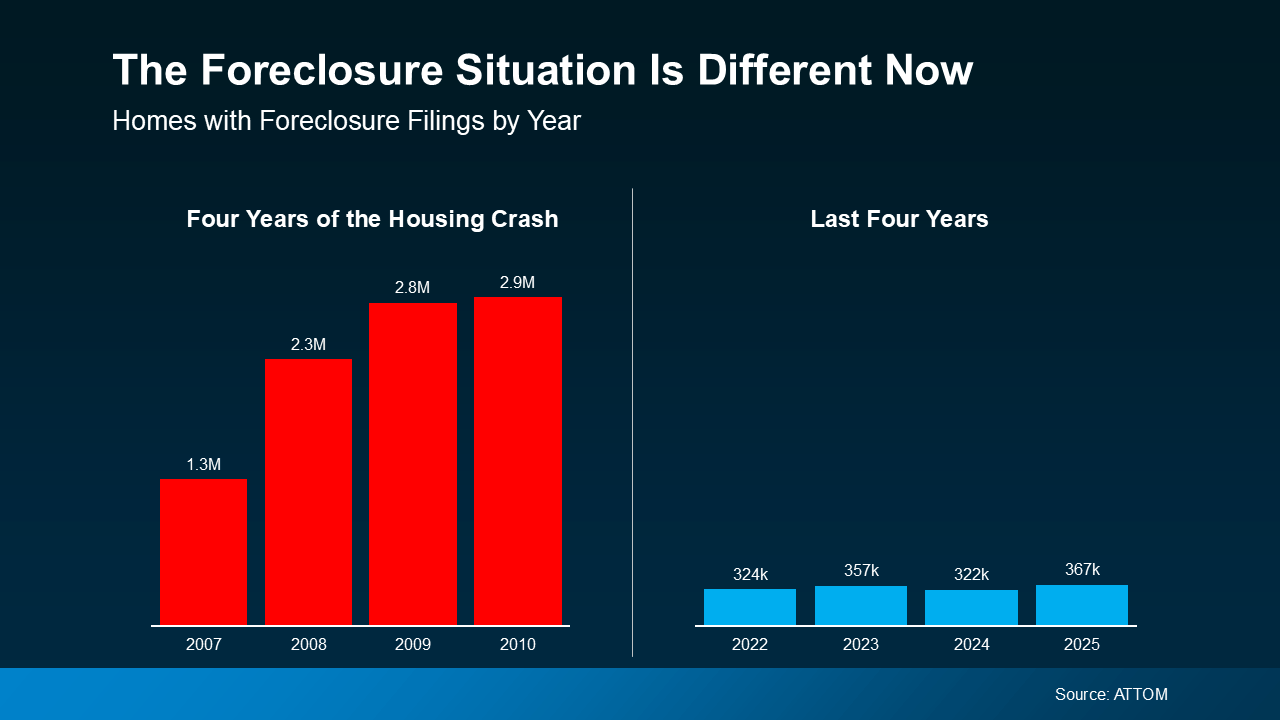

Yes — ATTOM reports foreclosure filings are up 32% year over year. That sounds dramatic, but context matters: it doesn’t mean we’re headed for another crash. The data tell the full story. Compare where we were during the last crash (the red in the graph below) to where we are now (the blue).

Even with the recent rise, we’re still a long way from any kind of crash. This isn’t a return to crisis, it’s just things getting back to normal.

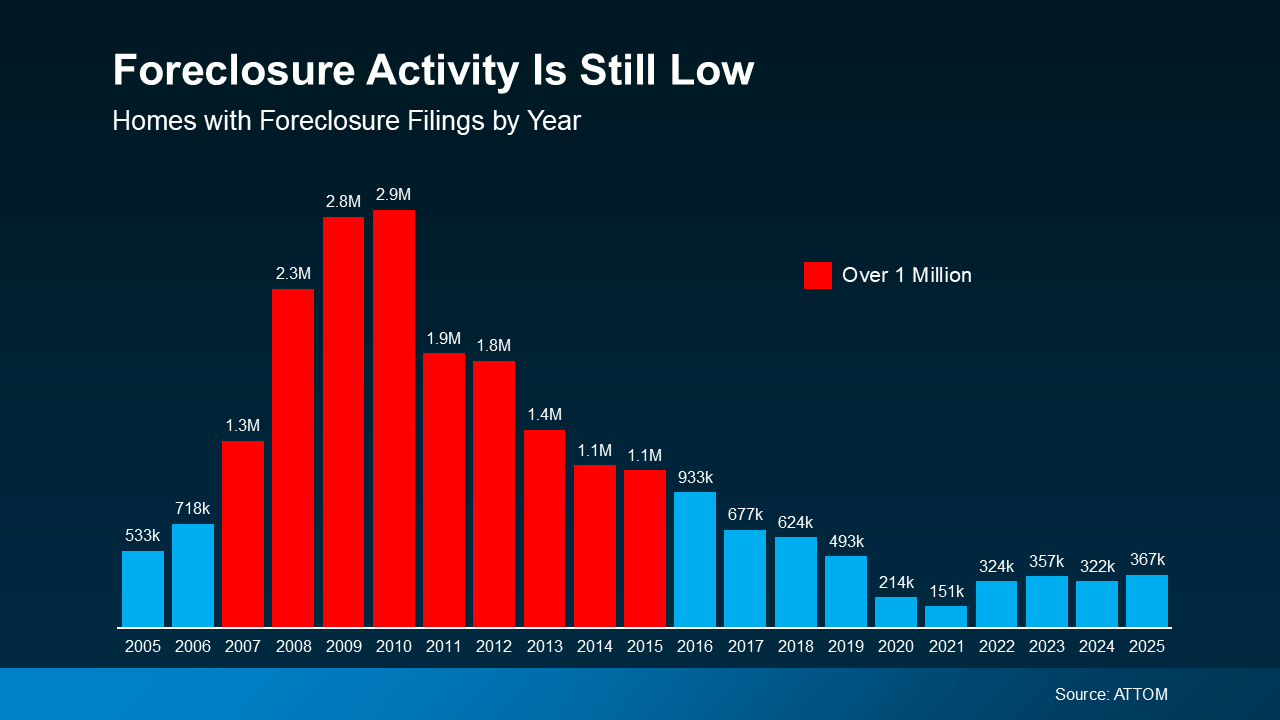

The chart tracks foreclosure filings back to early 2005. You can see the buildup to the crash and its fallout in red — those are the years when filings topped one million annually.

Look to the right and focus on the 2017–2019 period — the last truly normal years for housing. You’ll notice we’re just beginning to move back toward those typical market patterns, even with the recent uptick.

Rob Barber, CEO of ATTOM, puts it simply:

““Foreclosure activity increased in 2025, reflecting a continued normalization of the housing market following several years of historically low levels . . . While filings, starts, and repossessions all rose compared to 2024, foreclosure activity remains well below pre-pandemic norms and a fraction of what we saw during the last housing crisis . . . today’s uptick is being driven more by market recalibration than widespread homeowner distress, with strong equity positions and more disciplined lending continuing to limit risk.”

”

The word “normalization” there really matters. Yes, some homeowners are feeling pressure from economic and financial forces, but this isn’t a surge of distressed properties. Despite the headlines, it’s not a widespread crisis.

Today’s uptick isn’t cause for alarm — it’s just things getting back to normal.

Why This Isn't a Repeat of 2008

Even though the last housing crash still influences how many people read today’s headlines, this market is different.

Lending standards are much stricter than they used to be.

Today’s borrowers are better qualified and more prepared.

And most homeowners are sitting on significantly more equity.

That equity piece really matters. Home prices have climbed a lot over the past five years, so many homeowners’ properties are now worth much more than what they paid. That gives most owners a solid financial cushion they can rely on if they need it.

Today, if someone hits hard times, they can often choose to sell their home—and might even come away with cash—rather than go through foreclosure. That’s a big difference from 2008, when many homeowners owed more than their houses were worth.

Bottom Line

Foreclosure activity is ticking up, but it’s still within a normal range and far from the worst of past downturns. Sensational headlines can make things seem scarier than they are. That’s why having a trusted real estate expert to turn to matters—someone who can explain what’s really happening and help you make smart decisions.

If a news story or social post about housing worries you, get in touch — we’ll help you understand the context and whether it actually affects you.