You've probably been wondering lately, "Is it really a good time to try and buy a home?"

With home prices being high and mortgage rates staying stubborn, renting might feel like the safer option these days—or even your only option. It’s understandable to feel that way. Buying a home today might not be the best fit for everyone, and that’s okay. The key is to buy a home only when you’re truly ready and able, and when the timing works for you.

But here’s the important point about renting.

It might seem like a good idea right now—and in some places, renting could even be cheaper each month than owning a home—but in the long run, it could end up costing you more.

A recent survey by Bank of America revealed that 70% of people looking to buy a home are concerned about the impact of long-term renting on their future. Their worries are definitely valid.

It might feel like owning a home is just a distant dream, but with a solid plan and consistent effort, you can make it a reality. Plus, homeownership can bring significant financial advantages in the long run.

Homeownership Builds Wealth Over Time

Buying a home goes beyond just finding a place to live; it's also an important move in growing your future wealth.

Home prices usually go up over time, so if you wait to buy, it’s likely to cost you more down the road. Even in markets where prices might be dipping right now, the long-term trend shows that prices tend to rise overall.

As home values go up, your equity increases if you own a home. Equity is simply the difference between what your home is worth and what you still owe on it. Every time you make a mortgage payment, that equity builds. Over time, it contributes to your overall net worth.

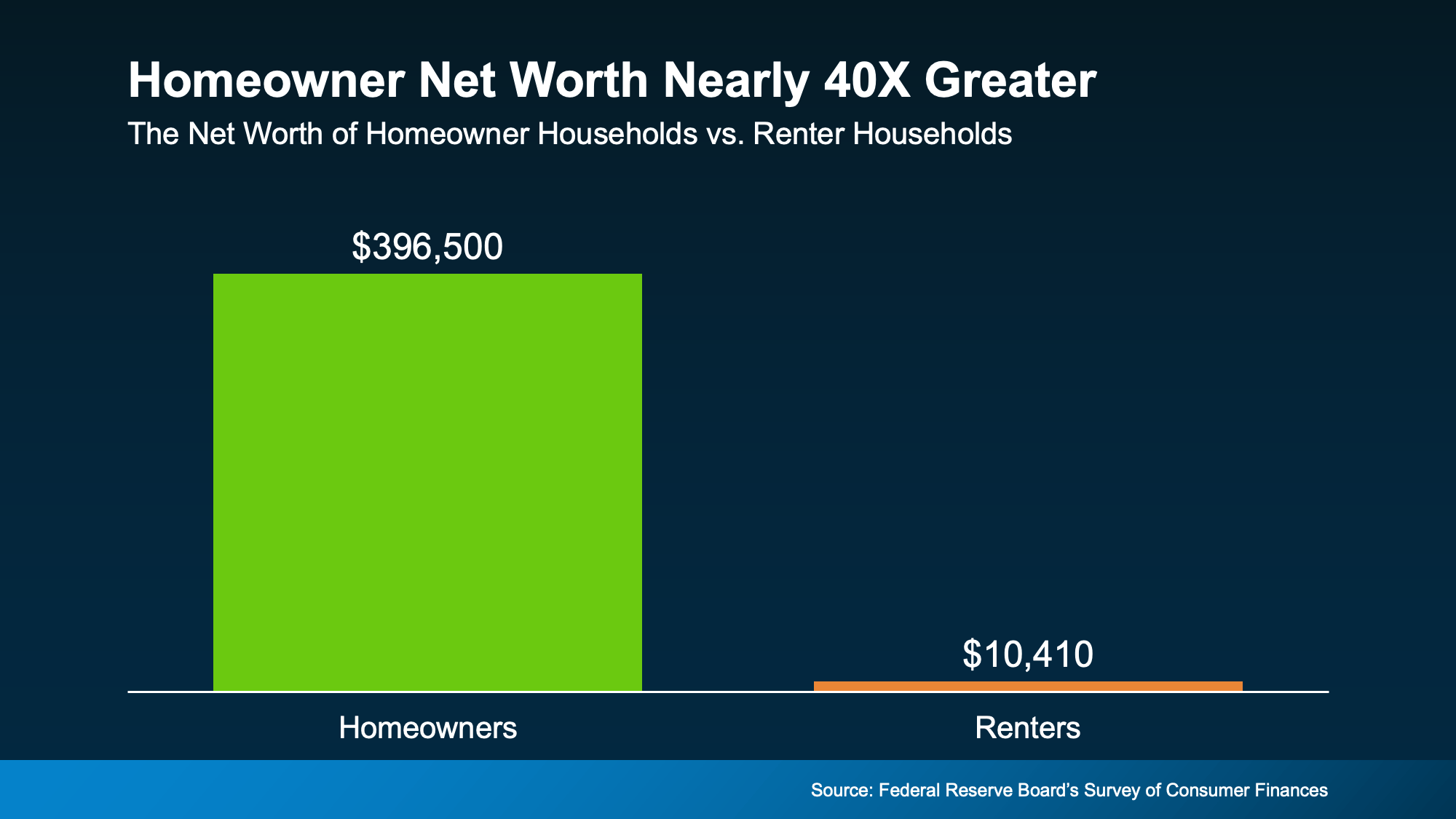

The typical homeowner's net worth is almost 40 times that of a renter. That's a significant gap, and the figures in the visual below clearly illustrate this difference.

It's one of the main reasons that Forbes highlights.

““While renting might seem like [the] less stressful option . . . owning a home is still a cornerstone of the American dream and a proven strategy for building long-term wealth.”

”

The Biggest Downside of Renting

Renting often feels like an easier option in the short term because you have lower monthly payments, fewer responsibilities, and no long-term commitments. However, if you look at the long run, it can really add up to be a tough pill to swallow.

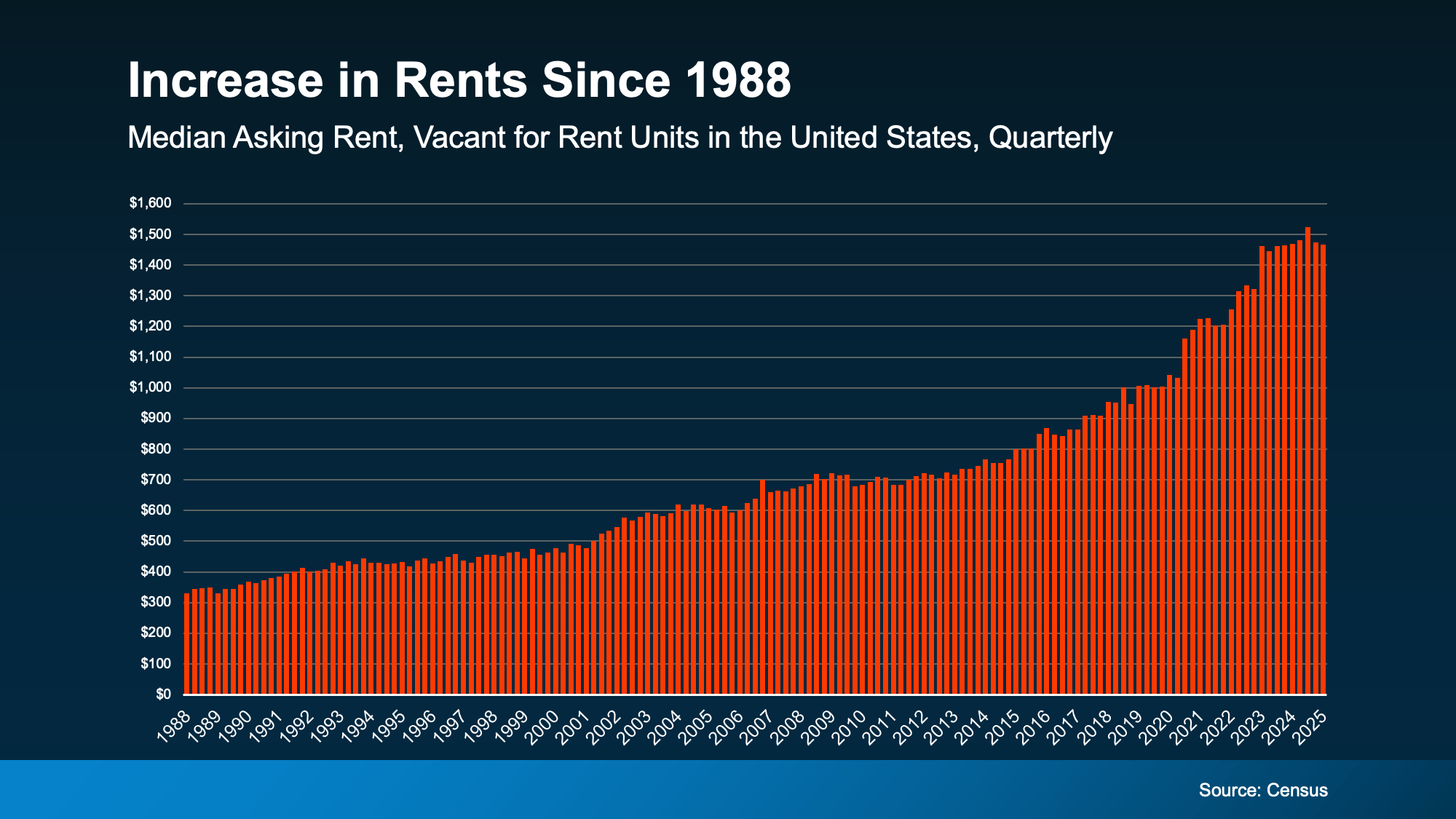

For years, both home prices and rent have been on the rise. Recently, rent has been pretty stable, but if you look back, you can see that the general trend has been upward. This makes it tougher than ever to save for a home.

Financial uncertainty can really take a toll. According to the same Bank of America survey, 72% of potential buyers expressed concern that increasing rent might impact their immediate and future financial situations.

Renting doesn’t help you build wealth. When you pay rent, that money isn't something you’ll get back later. Instead, it goes toward your landlord’s mortgage, not your own.

Whether you’re renting or owning, you’re essentially paying a mortgage. The real question is: whose mortgage do you want to be contributing to?

Renting vs. Buying: What Really Matters

Consider it like this: When you rent, your money is spent once you make the payment. But with owning a home, those payments go toward building equity—similar to having a savings account that you can actually live in. Yes, buying a home brings some responsibilities, but it also offers long-term rewards that grow over time. That’s why having a solid plan is essential to achieving ownership.

Joel Berner, a Senior Economist at Realtor.com, shares his insights:

““Households working on their budget will find it much easier to continue to rent than to go through the expenses of homeownership. However, they need to consider the equity and generational wealth they can build up by owning a home that they can’t by renting it. In the long run, buying a home may be a better investment even if the short-run costs seem prohibitive.”

”

Bottom Line

Renting might seem more manageable right now, but in the long run, it could end up costing you more without contributing to your future goals.

If homeownership seems out of reach right now, you’re not the only one. The first step to moving beyond renting is creating a plan. Let’s connect to define your goals and look at your options, so you’ll be prepared when the right moment arrives.