If you have a 3% mortgage rate, you might feel uneasy about the idea of letting it go. Even if you've considered moving, that persistent question could be lingering in your mind: "Why would I give that up?"

When you ask that question, you might not realize you're prioritizing others over your own needs. Typically, people don’t move just because of their mortgage rate; they move out of necessity or desire. So, let’s change the approach and ask this instead:

What do you think the odds are that you'll still be living in your current home five years from now?

Take a moment to reflect on your life. Imagine where you'll be in the next few years. Are you considering expanding your family? Do you have adult children ready to leave the nest? Is retirement approaching for you? Or are you already feeling cramped in your current space?

If everything is going to stay the same and you really enjoy your current place, sticking around could be a great choice. However, if there's even a small possibility that you'll be moving in the future, even if it's not on the horizon right now, it’s a good idea to consider your timeline.

A year or two can really change the price of your next home.

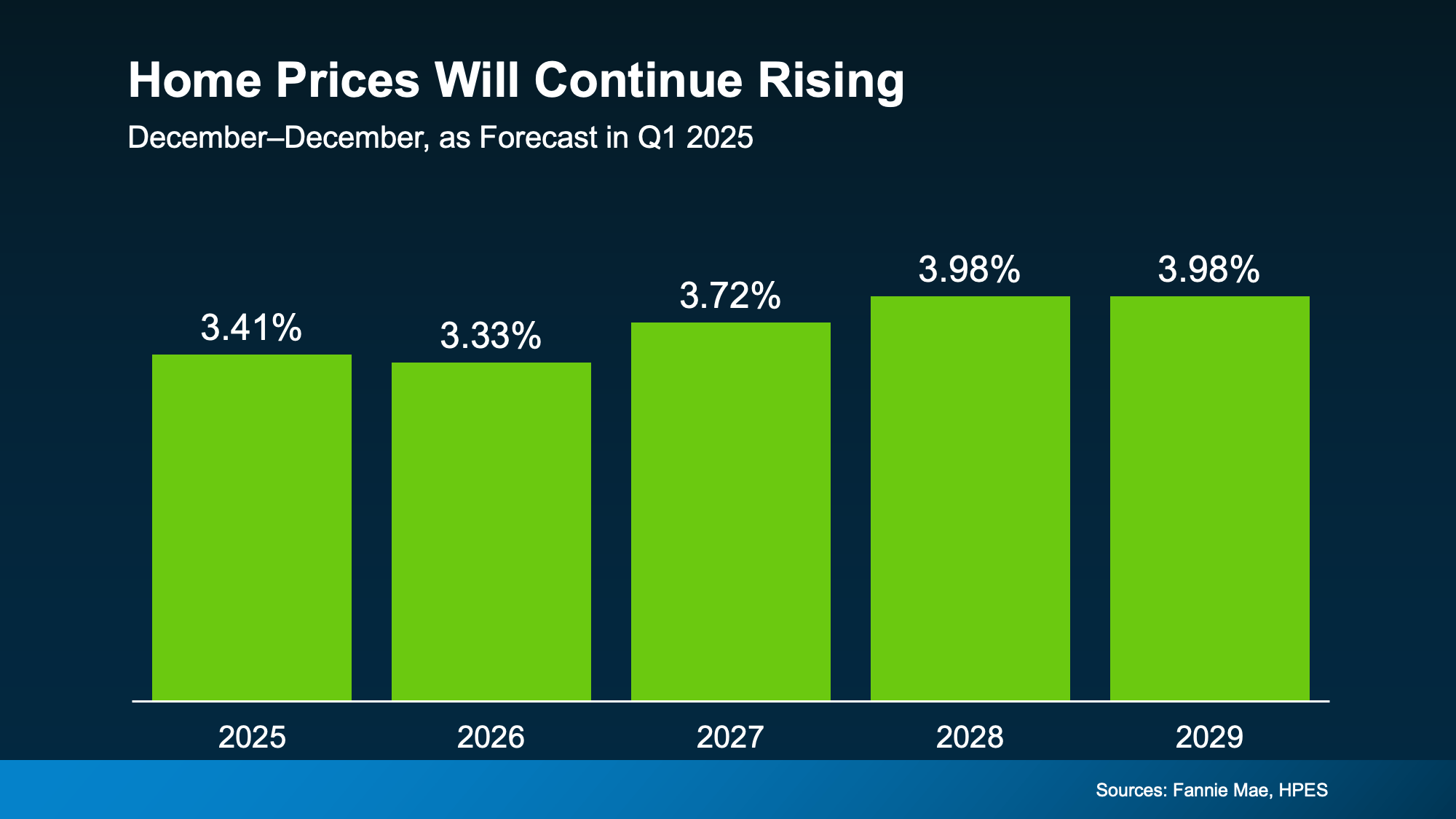

What the Experts Say About Home Prices over the Next 5 Years

Every quarter, Fannie Mae checks in with over 100 housing market experts to get their take on where home prices are headed. And the message is pretty clear: prices are expected to keep climbing through at least 2029 (check out the graph below).

Now, these projections aren’t saying we’ll see huge jumps every year—but they are still pointing to growth. Sure, some areas might have flatter prices, slower gains, or even small dips here and there in the short term. But zoom out a bit. Over time, home prices almost always go up. And even modest increases over the next five years can really add up.

Take this as an example—say you're planning to buy a home around the $400,000 mark. If you hold off and wait five years, based on what the experts are projecting, that same home could end up costing you almost $80,000 more than it would today (check out the graph below)

That basically means the longer you wait, the more you’ll likely end up paying for your future home.

If you think you might be moving soon, it’s a good idea to consider your timeline. You don’t need to rush into a move, but it can be beneficial to discuss your options now before prices go up. While rates are expected to decrease, the drop won’t be significant. If you’re hoping for the return of 3% rates, experts suggest that's unlikely to happen.

The question isn’t really “why should I move?” but rather “when is the right time?” The numbers show that waiting might not actually save you money. This is an important discussion to have with your trusted agent right now.

Bottom Line

Keeping that low mortgage rate is a smart move, but it can become a hurdle if it starts to limit your options.

If you're thinking about moving, even if it's a couple of years away, it’s a good idea to start crunching the numbers now so you can be prepared.

What price range are you interested in for these numbers? Let’s discuss it so I can explain how it all works. This way, you’ll have the information you need to make a smart decision about your timeline.