Renting often seems cheaper and easier than buying a home, especially these days. There’s no need to handle repairs, worry about property taxes, or stress over mortgage rates—you simply pay your rent and go about your day.

Here’s something that doesn’t get mentioned enough: renting doesn’t really help you build your financial future. On the other hand, homeowners build their net worth simply by owning their home.

If you’ve been questioning whether buying a home is still a smart move, the long-term numbers actually make it more straightforward than you might expect.

Renting vs. Owning: How the Costs Really Compare

Here’s a simple way to look at a big difference between renting and buying. When you rent, your monthly payment goes straight to your landlord, and that’s the end of it. But when you own a home, a portion of your payment actually builds your equity—that’s the value you gain as your home appreciates and as you pay down your mortgage. So, owning means you’re investing in your future, not just paying for a place to live.

Sure, renting might look cheaper on the surface right now, but keep in mind that it comes with a long-term downside: you’re not growing your own wealth. And that missed opportunity is more significant than you might think.

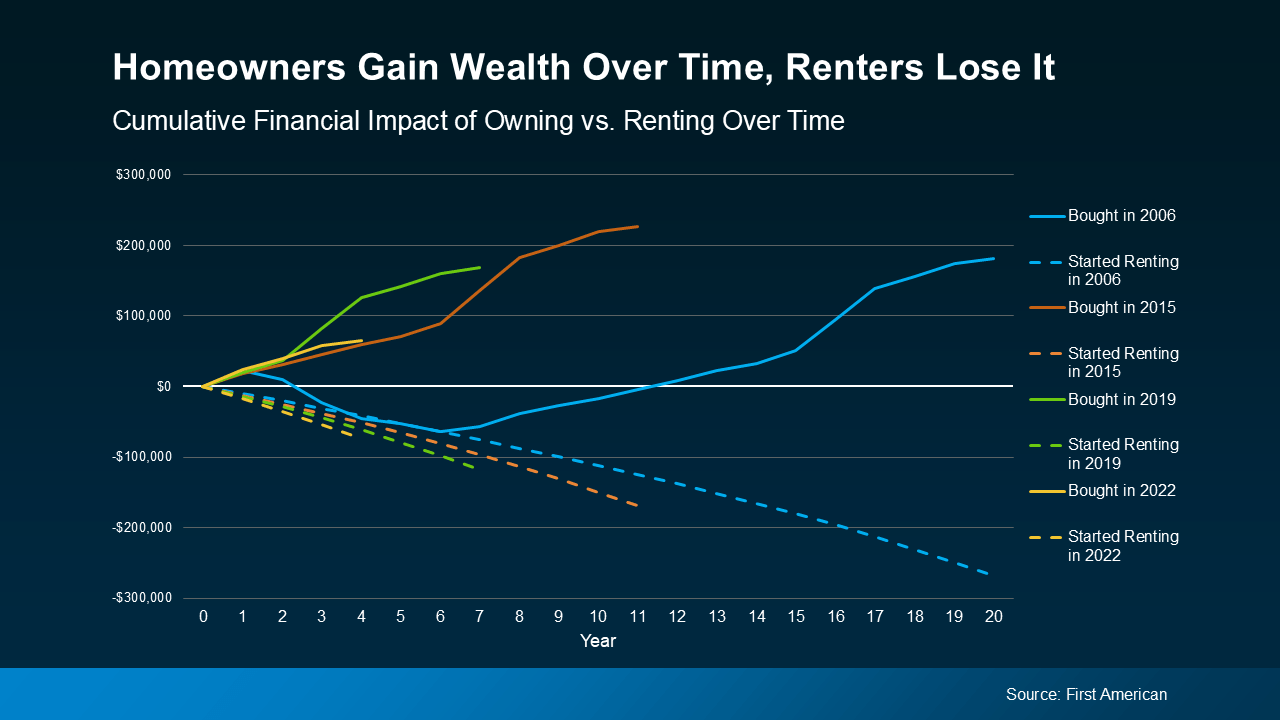

First American took a close look at the financial ups and downs of renting versus owning a home over the long haul. They compared the costs you face—like mortgage payments, property taxes, insurance, repairs, and maintenance—with the equity you build up from home price appreciation and paying down your mortgage. They ran this analysis across several different time periods to see if the results held steady.

2006 — right at the beginning of the housing bubble

2015 — about a decade ago

2019 — just before the pandemic, when the market still felt “normal”

2022 — the year mortgage rates really started to climb

Let’s break down what this means. Each color stands for a different key time frame. The solid lines track how much a homebuyer has invested over time and show how their net worth actually increased the longer they stayed in their home. On the other hand, the dashed line shows what happens with a renter’s investment. Over time, renters keep putting money into rent but don’t see any financial gain from it.

The key point is clear: owning a home over time helps you build wealth, while renting doesn’t offer the same financial growth.

Homeowners still win. Even when you add in all the extra costs that come with owning a home—like insurance, repairs, and property taxes—the numbers still favor buying over renting. And that held true no matter which time period First American analyzed.

On the other hand, renters paid their rent but didn’t build any long-term financial value from it. This held true no matter what time period the study looked at.

That doesn't mean buying is always better than renting right away. But the longer you stay in your home, the more your wealth tends to grow compared to renting.

Affordability Is Starting To Improve

You’re probably still wondering, “Okay, but buying feels out of reach for me right now.” Fair.

The last few years have been tough for buyers, but the situation is beginning to improve. Mortgage rates have dropped this year, home prices are easing up, and incomes are going up. Zillow reports that monthly payments are a bit more manageable than they were at this time last year—not by a huge margin, but enough to make a noticeable difference.

No, buying a home hasn’t suddenly become easy. But it is a bit easier now than it was just a few months ago. And over time, history proves that it’s worth the effort.

Bottom Line

Renting can seem cheaper right now, but owning a home is what really helps you build wealth over time. Plus, as affordability begins to get better, buying a home might be more within reach than you realize.

If you’re wondering what buying a home might look like for you, let’s chat. We can explore your options together, with no pressure.