Many buyers are holding back right now, adopting a “wait and see” approach. They’re keeping an eye on mortgage rates that are just above 6% and thinking, “I’ll make a move once rates dip into the 5% range.” After all, everyone wants to lock in a lower rate if they can.

Here’s the thing: that 5.99% rate might not actually save you as much money as you expect.

Affordability is definitely still a challenge, no doubt about it. But the good news is, the market has actually given smart buyers a bit of an advantage. Mortgage rates have been dropping over the last few months, and the savings from that decrease are more significant than you might expect.

How Much You’ve Already Saved, Without Realizing It

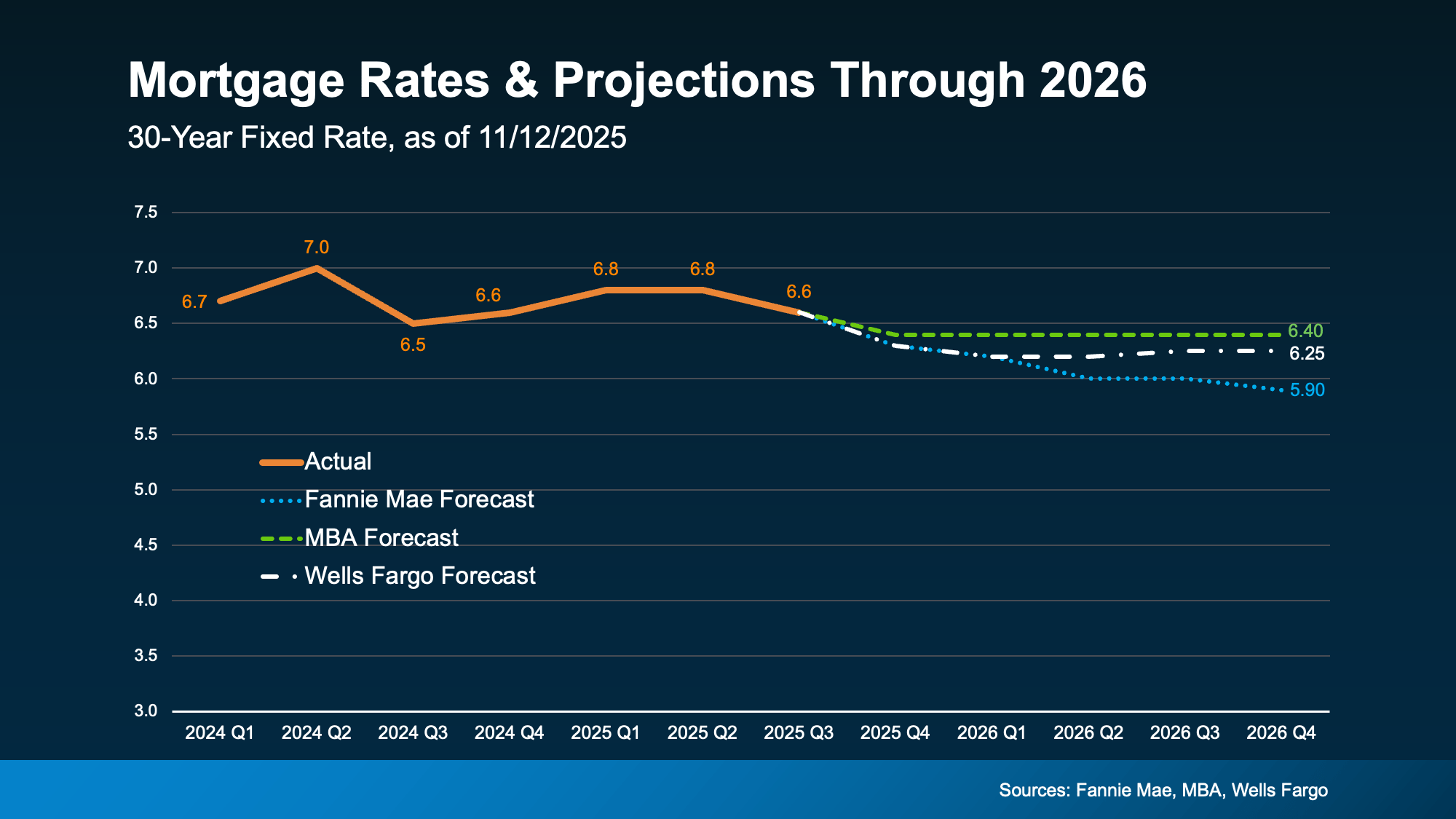

Let’s break it down with some real numbers. Back in May, rates hit their highest point for the year, just over 7%. Since then, they’ve been gradually coming down and are now in the low 6% range. It might not seem like a huge difference, but that drop actually means significant savings when it comes to your mortgage payments.

Data from Redfin shows that the average monthly payment on a $400,000 home has dropped by nearly $400 since May.

If you’re buying a home now, you’re actually saving hundreds of dollars each month compared to earlier this spring. That’s a significant amount of money that can truly make a difference for buyers who put their plans on hold, thinking homeownership was out of reach.

It might be tempting to hold off longer in hopes of getting bigger savings, but that’s a risk that could end up costing you. Here’s what you need to know.

Where Experts Say Rates Are Headed

Most experts agree that mortgage rates will probably hover around the same levels throughout 2026. So, it’s unlikely we’ll see rates drop much lower than they are now. In fact, only one expert predicts that rates might dip into the upper 5% range next year.

Even if rates drop below 6%, the extra savings you’re hoping for probably won’t make as big a difference as you think.

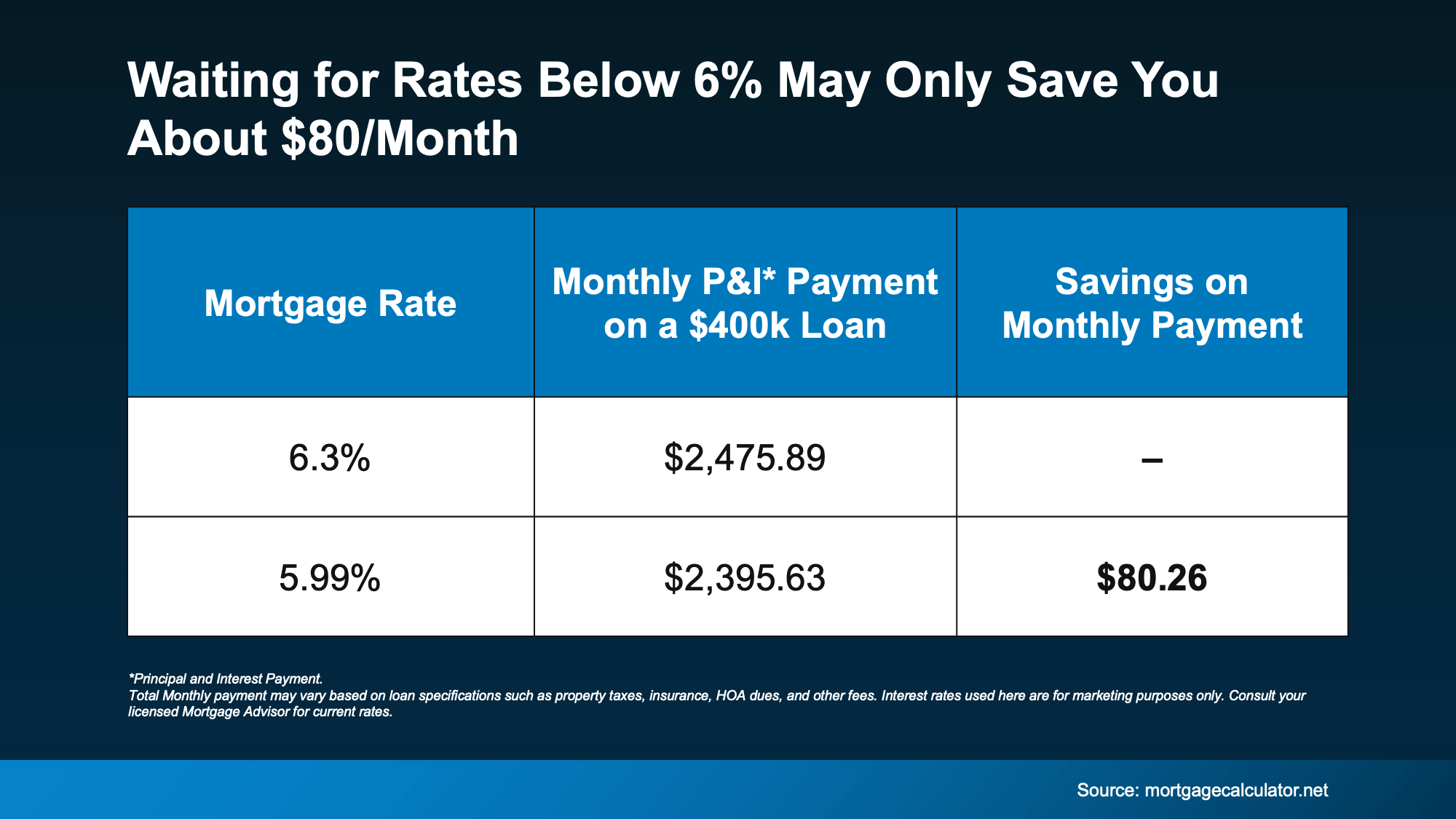

The Real Math Behind a 5.99% Rate

Let’s simplify it. If mortgage rates drop to 5.99% from recent levels, that’s roughly an $80 monthly savings on an average-priced home. Of course, the exact amount varies depending on your home price and the rate your lender offers you.

Eighty dollars. That’s all it is. For most families, it’s about the cost of one dinner out—or one dinner in if you’re ordering delivery. It’s not a huge game changer for most buyers. But when you think about the nearly $400 in savings we’ve already seen compared to when you stopped your search back in the spring, that could make a real difference.

Here’s the question you should be asking yourself:

Is waiting really worth saving an extra $80?

While you’re waiting for that slight drop, the bigger chance could be passing you by.

When Rates Fall, Competition Follows

At the moment, there are plenty of homes available, sellers are open to negotiating, and there’s less competition from other buyers. However, when interest rates drop below 6%, buyer attitudes will change, and the market will look very different.

The National Association of Realtors (NAR) says that if mortgage rates reach 6%, around 5.5 million more households could afford the median-priced home. Even if just a small portion of those people decide to buy, it could result in hundreds of thousands of new buyers entering the market.

That means more buyers going after the same homes, which can drive prices up—possibly so much that any extra savings you hoped to get won’t actually make a difference.

If you’re holding out for rates under 6%, remember that saving an extra $80 might not make a big difference in the long run.

Bottom Line

You don’t need to wait for rates to drop to 5.99%. You can make a move—and save money—today. So, ask yourself this: Would you really let $80 stop you from buying a home?

If you come across a home you really like and the numbers add up, moving quickly could be your best move. Let’s take a look at your finances so you know exactly where you stand in today’s market.